In his magisterial 2005 history A Nation of Realtors, Jeffrey Hornstein laid out the country-shaping effect of 20th-century housing policy. In the decades following the Great Depression, the Federal government—as well as states and cities—subsidized the creation and consumption of single-family homes. The American dream’s most important archetype became buying a home. “Americans,” Hornstein wrote, “particularly white Americans, came to think of themselves as inhabiting a classless society, composed of one big ‘middle class,’ its membership defined to a large degree by actual or expectant homeownership.”

Recently, however, we’ve lost the plot on the classic life arc of yesteryear. In places where real estate is cheap, there aren’t many good jobs. In the places with lots of jobs, primarily coastal cities, the real estate market has gone absolutely haywire. The most recent evidence of this remarkable change comes in a new report by the real estate firm Unison. The company, which provides financing to homebuyers by “co-investing” with them, calculated how long it would take to save up a 20-percent down payment on the median home in a given city by squirreling away 5 percent of the city’s gross median income per year.

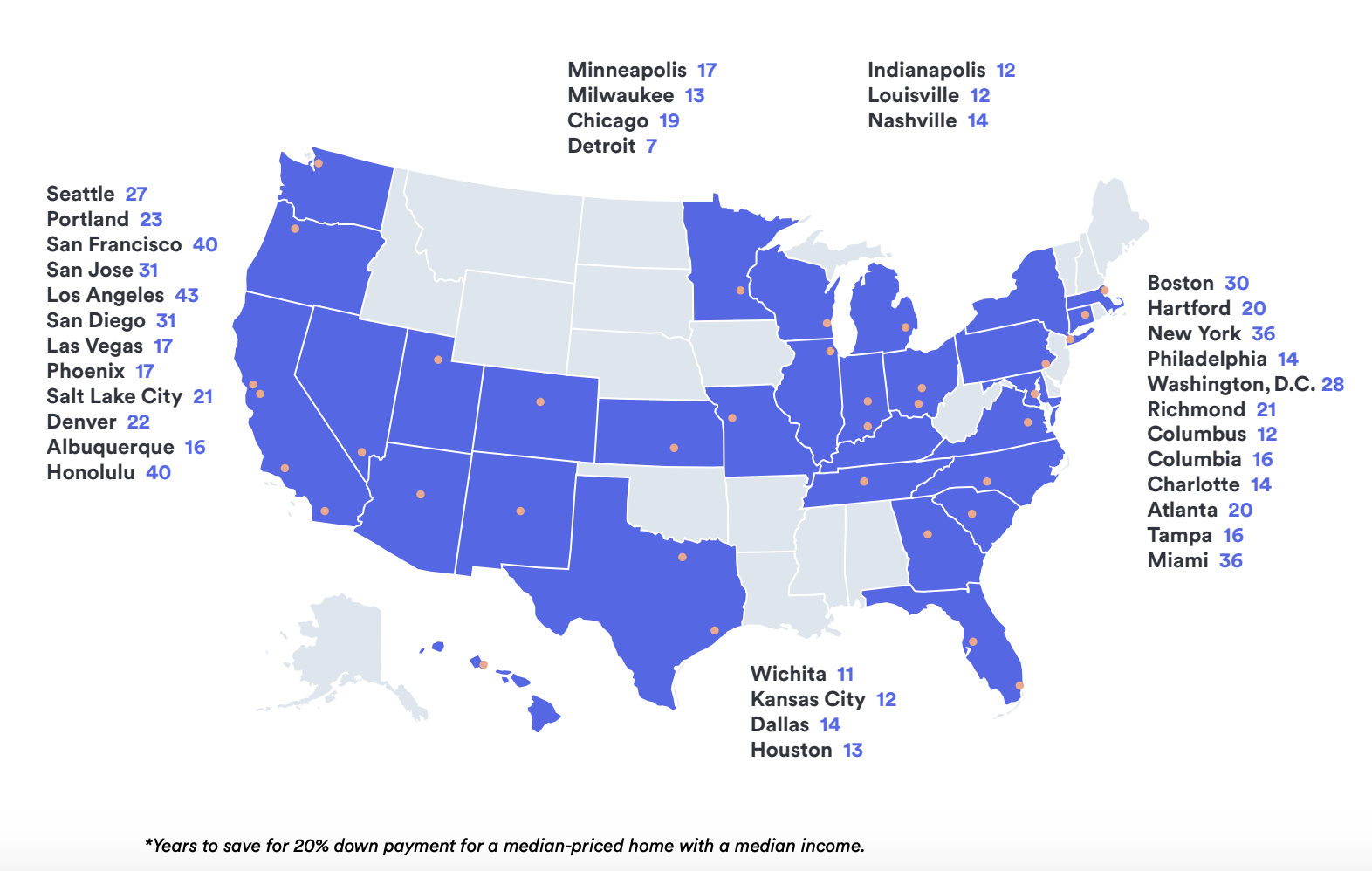

Nationally, the gap between income and home value has been rising. Using Unison’s methodology, it only took 9 years to save up a down payment in 1975. Now, it takes 14.

But the aggregate numbers make the decrease in access to the real estate market seem gradual, albeit troubling, and underplay the spikiness of the country. In Los Angeles, it would take 43 years to save up for a down payment. In San Francisco, 40. San Jose and San Diego, 31. Seattle and Portland, 27 and 23 respectively. In the east, New York and Miami topped the list, at 36 years to save up that down payment. Only Detroit, at 7 years, was under the national average from 1975.

Generationally, this has huge consequences. Imagine you’re a 30-year old in Los Angeles with the median income. By Unison’s math, you can imagine buying a home at 73. For young people in high-opportunity metro areas, the route to home ownership is basically blocked without the help of a wealthy family member or some stock options. Meanwhile, older people who bought under much more favorable circumstances have seen their equity stakes grow and grow and grow.

One part of the problem is easy to identify: housing scarcity. The Bay Area has become the poster child for this factor. More than half a million jobs were created between 2010 and 2017, but only 76,000 housing units were built. You don’t have to be a market fundamentalist to see how that could cause problems. And indeed, the median single-family home price in San Francisco is more than $1.6 million, and close to $1 million for the whole nine-county Bay Area region. (The median price for all types of housing units in the whole region was $830,000.)

The simplest way to read these numbers is that the real estate market in job-rich cities like San Francisco does not work for the vast majority of young people. That’s why so many housing debates in big coastal cities feel like generational warfare. Policies—like changes in restrictive zoning or building lots of new multifamily units—that could lower home prices are promoted heavily by younger people, who would like to participate in a less insane real estate market. At the same time, many homeowners, and the city officials they elect, see propping up real estate values as what the government does.

And then, of course, there is the fact that even as old-fashioned biological explanations of racial hierarchy fell out of fashion, white homeowners continued to pass and uphold racist housing policies, by shifting their rationale to property values, as David Freund showed in his book Colored Property. “Federal policy promoted restrictive zoning and created a flush new market for housing that required racial segregation, yet encouraged whites to believe that it was the free market, not racial prejudice or government policy, that set the rules of competition,” Freund wrote, “that the exclusion of minorities was not about race per se but about the principles of real estate economics and homeowners' rights to control their communities.”

Many of these policies served to restrict the number of affordable homes. So, now, decades later, in many cities with good economies that have drawn new residents, increased demand has not been met with commensurate supply. Young people of all races are experiencing the consequences of these policies, but given the compounding nature of wealth, the relative inaccessibility of home prices is an ongoing disaster for the racial wealth gap.

In states like California, which has limited the reassessment of property taxes since 1978, young people shoulder a double burden. Not only must they try to buy homes under much more difficult circumstances than their parents, they also must pay higher property tax rates than them, while local governments receive less revenue (and provide less service) than they might have. At the same time, getting rid of this tax subsidy for older homeowners would bounce many from their homes, as the taxes on the real value of their homes exceeds what many people on fixed incomes could pay.

There are obviously many reasons why coastal housing markets have gone so bonkers. But it is an ironic twist that residential property, which once served as the bedrock for American capitalism, has become the most obvious sign for young people that something is deeply wrong with the markets.

from Technology | The Atlantic http://bit.ly/2IL7h3k